The Short Answer: Homeowners can finance a pool through home equity loans, HELOCs, cash-out refinancing, personal loans, or pool builder financing, with each option offering different rates, terms, and trade-offs based on your equity position and credit profile.

Adding a swimming pool or hot tub to your backyard can be a significant investment, and most homeowners need financing to make it happen. Pool costs can range widely depending on the pool type, size, features, and location.

Understanding your financing options helps you make a smart decision that fits your budget and long-term financial goals. The right financing approach depends on your equity position, credit score, risk tolerance, and how much flexibility you need during the pool project.

How Much Does a Pool Cost?

Before exploring financing options, it helps to understand what you are likely to spend. Above ground pools typically offer a more affordable entry point. Inground pools represent the largest investment, with costs ranging from:

- Concrete Pools: $50,000 to $100,000 or more

- Fiberglass Pools: $45,000 to $85,000

- Vinyl Liner Pools: $35,000 to $65,000

These ranges vary significantly based on size, depth, materials, features like waterfalls or lighting, and your geographic location.

Additional Costs

In addition to financing the pool itself, a budget for additional costs is required, including decking, fencing, landscaping, permits, and electrical work. Planning for these expenses from the start helps you avoid financial strain down the road.

Other ongoing costs like maintenance, chemicals, cleaning, utilities for pumps and heaters, increased homeowner’s insurance, and equipment replacement also add to the total cost of ownership.

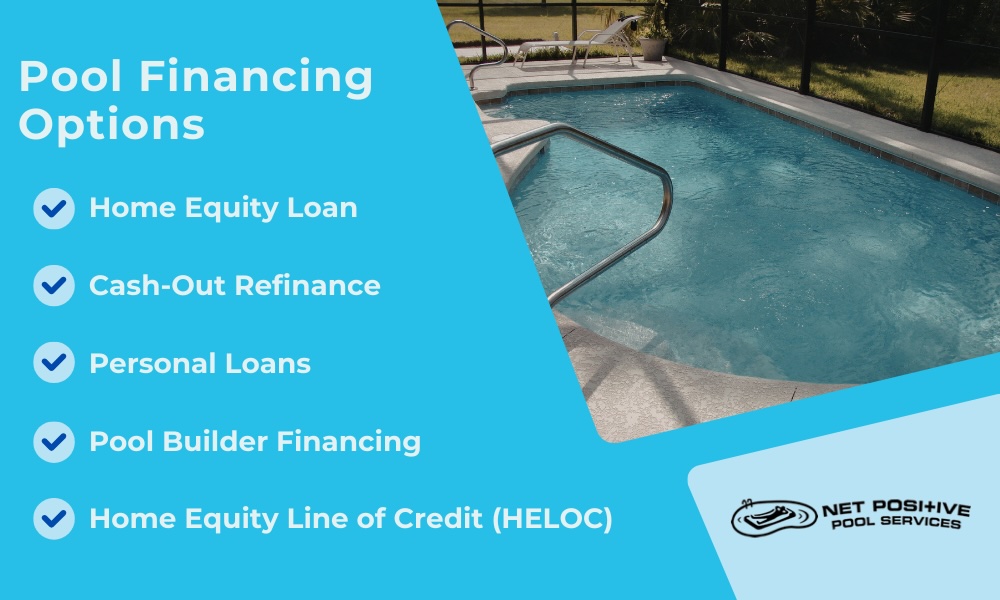

Common Pool Financing Options

Homeowners have several ways to finance a pool, each with different requirements, rates, and trade-offs. Understanding these options helps you choose the approach that best fits your situation.

Home Equity Loan

A home equity loan uses your home’s equity as collateral. You receive a lump sum and repay it over a fixed term at a fixed rate. This option works well for homeowners with significant equity who want predictable monthly payments. These competitive interest rates are generally lower than unsecured options, and the interest may be tax-deductible since the funds are used for home improvement.

Home equity loans offer lower interest rates, fixed payments, and potential tax deductibility. However, they use your home as collateral, involve closing costs, and have a longer approval process.

Home Equity Line of Credit (HELOC)

A HELOC is a revolving credit line secured by your home’s equity. You can draw funds as needed during a draw period, then repay over time. HELOCs typically have variable interest rates, which means your payments can change. This option offers flexible terms for homeowners who are unsure of the total project cost or want to pay for the pool in stages.

HELOCs allow you to pay interest only on what you borrow, but variable rates can increase over time, and your home remains at risk if you cannot repay.

Cash-Out Refinance

Cash-out refinancing involves refinancing your mortgage for more than you currently owe and taking the difference in cash. You replace your existing mortgage with a new, larger one, and the new rate and term apply to the entire pool loan. This can be attractive if you can secure a lower interest rate than your current mortgage, but it extends your mortgage term and resets your loan balance.

This option can potentially lower your overall interest rate and consolidate payments, and you extend your mortgage term while resetting your loan balance. However, closing costs can be significant.

Personal Loans

These unsecured loans are not tied to your home. You borrow a fixed loan amount and repay it over a set term. Interest rates are typically higher than secured loans because there is no collateral, but approval is often faster. Personal loans work well for homeowners without significant equity or those who prefer not to use their home as collateral.

Personal loans require no collateral and offer faster approval with fixed terms, but interest rates are higher, repayment periods are shorter, and borrowing limits may be lower.

Pool Builder Financing

This is arranged through or offered by the pool installation company. Builders often partner with lenders or offer in-house payment plans. Terms vary widely and may include promotional rates or deferred interest. While convenient, you should always compare these offers against other financing options.

Pool builder financing is convenient and may include promotional rates, but you may not get the best available terms.

Credit Cards

These can be used for smaller portions of a project, but high interest rates make them a poor choice for large balances carried over time.

Credit cards offer immediate access but are expensive for large balances.

Factors to Consider When Choosing Pool Financing

Interest Rates & APR

Get quotes from multiple lenders and loan types, understand the difference between fixed and variable rates, and calculate the total interest you will pay over the life of the loan. A lower monthly payment does not always mean a better deal if you end up paying significantly more in interest over time.

Loan Terms & Monthly Payments

Longer terms mean lower monthly payments but more total interest paid. Shorter terms mean higher payments but less overall cost. Choose terms that fit comfortably in your monthly budget without overextending your finances.

Fees & Closing Costs

Ask about origination fees, closing costs, and prepayment penalties. Factor these into your comparison and request full fee disclosure from every lender before committing.

Collateral Requirements

These affect both your interest rate and your risk. Secured loans (home equity) typically offer lower rates but put your home at risk if you cannot meet the repayment terms. Unsecured loans (personal loans) have higher rates, but do not use your home as collateral

Credit Score

Your credit score affects the rates and terms you qualify for. Check your credit before applying and address any errors or issues. Remember that multiple loan applications in a short period can temporarily affect your score.

Tax Implications

Interest on home equity loans may be tax-deductible if used for home improvements. Consult a tax professional to understand how different loan options affect your specific situation

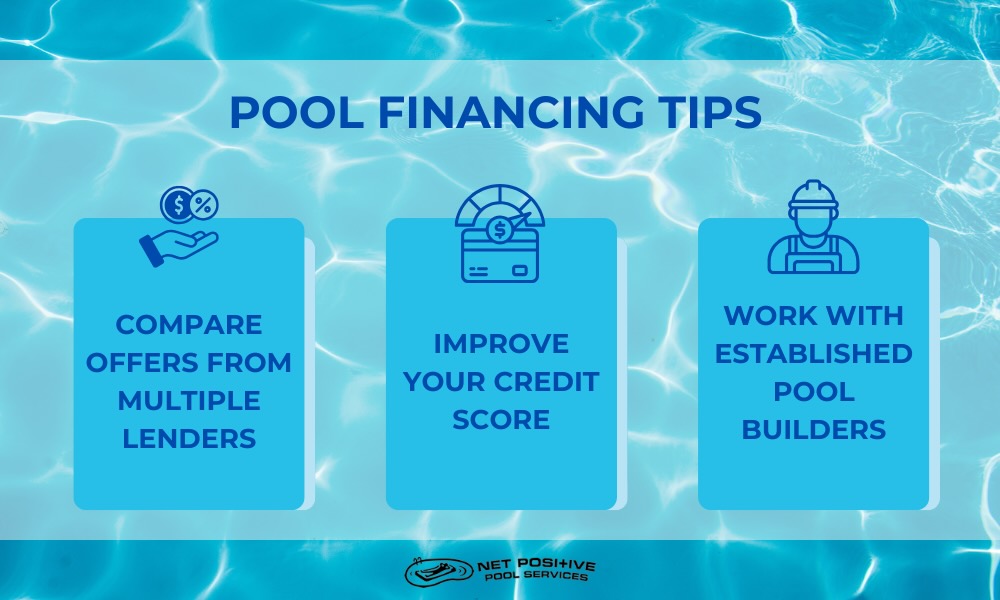

Tips for Getting the Best Pool Financing Terms

Compare Offers

Shop around and get quotes from multiple lenders, including banks, credit unions, and online lenders. Compare APR, fees, and total cost rather than focusing only on monthly payments. Do not settle for the first offer you receive, as rates and terms can vary significantly between lenders.

Improve Your Credit Score

If possible, pay down existing debt, correct any errors on your credit report, and avoid opening new credit accounts in the months leading up to your application. Even a modest improvement in your credit score can result in better rates and terms.

Consider Total Project Cost

Get detailed quotes from pool builders that include all costs such as permits, landscaping, fencing, and equipment. Borrow enough to complete the entire project rather than taking out multiple loans, which can be more expensive and complicated.

Read the Fine Print

Watch for prepayment penalties that could cost you if you pay off the loan early, balloon payments, and rate adjustments.

Work with Established Professionals

When choosing a lender and builder, make sure to verify their credentials, check references, and avoid high-pressure sales tactics or deals that seem too good to be true.

Questions to Ask Before Financing a Pool

Before committing to financing, ask important questions to everyone involved:

Lenders

- What is the APR and is it fixed or variable?

- What fees are included, such as origination, closing, or prepayment penalties?

- What is the total cost of the loan over its full term?

- How long is the approval process?

Pool Builders

- What is included in the quoted price?

- Are there potential additional costs that could arise during construction?

- Do you offer financing, and what are the terms?

- What is the payment schedule during construction?

Yourself

- Can I comfortably afford the monthly payment without straining my budget?

- Am I prepared for ongoing pool maintenance costs?

- Does this fit my long-term financial goals?

- What happens if my financial situation changes unexpectedly?

Finance Your Pool with Net Positive

Financing a pool is a significant decision that requires careful consideration of your options. Take time to compare multiple financing options, understand total costs including fees and interest, and factor in ongoing pool expenses beyond installation.

Work with reputable lenders and pool builders who are transparent about terms and pricing. With the right preparation and financing approach, you can enjoy your new pool or pool renovation for years to come.